This is part of The New Cost of Everything, a five-part series on how I see AI creating macro trends. This is the final post. You can read it on its own, but it also helps if you read all of them together. Start at Post 1 if you want the full arc.

The Pattern

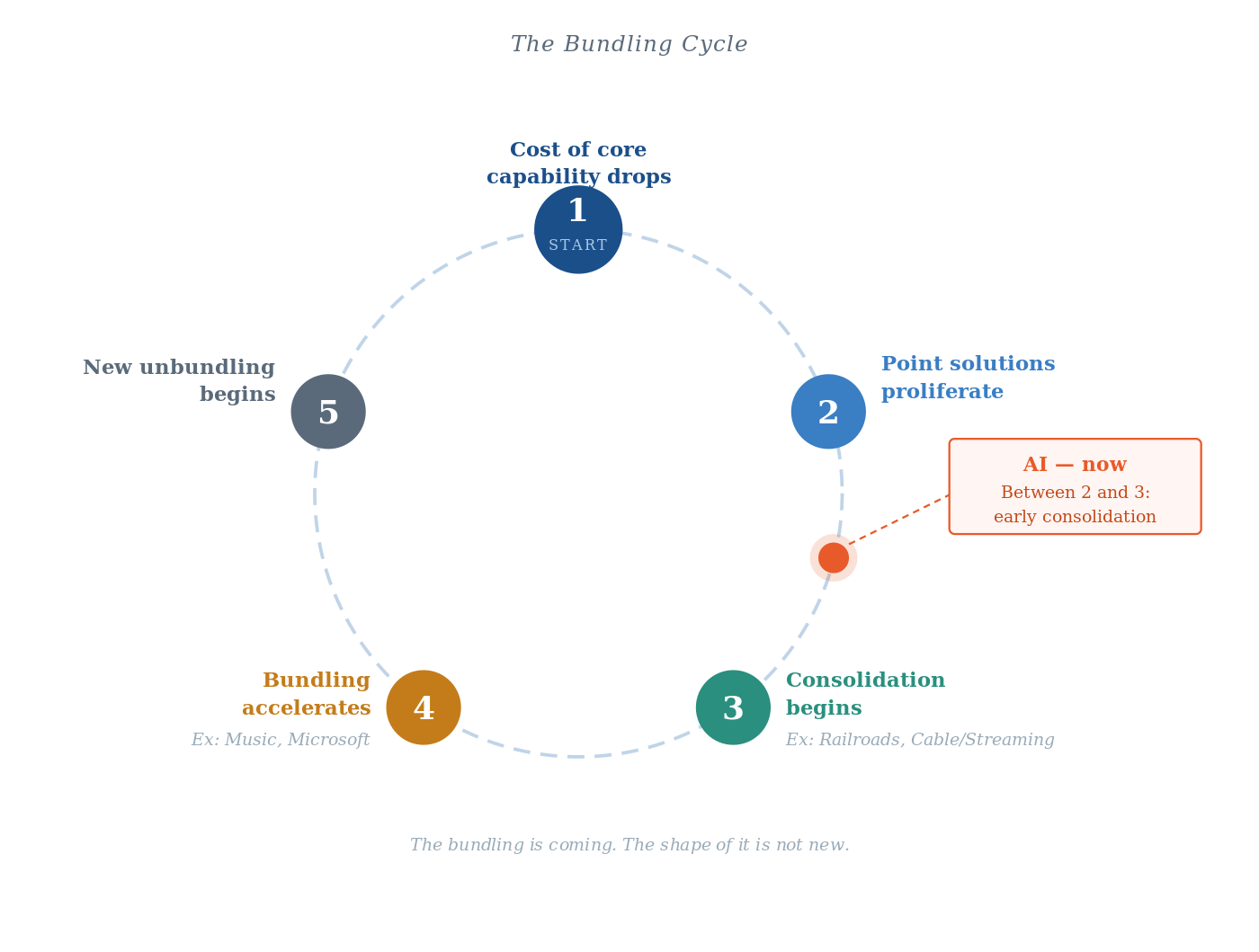

In 1800, moving goods in America required wagons on rough roads or boats on rivers. Slow, expensive, geographically constrained. Steam power changed the physics. By 1890, most shortline railroads had been consolidated into twenty trunk lines, and the vast majority of Midwestern farms were within a single day’s wagon haul of a railway.1

But railroads carried more than just freight. They bundled the telegraph into their right-of-way using the same poles, the same routes, the same infrastructure. Congress recognized the inseparability: the Pacific Railroad legislation explicitly linked railroad and telegraph. The bundle wasn’t just trains. It was trains, telegraph, and the rate-setting power that came with owning the network. Every point solution that depended on rail — such as independent freight haulers, small refineries, regional telegraph operators — eventually got absorbed, displaced, or regulated out.

Rockefeller saw this and he didn’t compete with the railroads. He negotiated favorable shipping rates with them, merged Cleveland refineries, and used the network to consolidate the petroleum industry. Standard Oil’s power came from understanding that whoever controlled the infrastructure controlled the economics of everything that moved through it.

Time for a different tune: music. Music ran the same sequence, albeit faster. Physical albums were the bundle: twelve songs, one price, the record label’s curation determining what you heard. Then digitization collapsed the cost of distribution. iTunes unbundled the album into individual tracks — you bought the song you wanted, not the ten songs around it. The album as a product nearly died. Then Spotify arrived and re-bundled everything: all the music, one subscription, priced below what a single album used to cost. The cycle ran completely in about twenty-five years. Bundle, unbundle, re-bundle.

Cable television ran the same sequence. Local broadcasters had unbundled from national networks. Cable bundled them back together and added more: ESPN, CNN, HBO, MTV — each a point solution, packaged into a single subscription. Then Netflix arrived and unbundled again. Then Netflix started acquiring sports rights. Then Disney bundled Disney+, Hulu, and ESPN+ into a single subscription at a combined price below what any one of them had charged alone.

Microsoft ran the fastest version. It bundled the browser into Windows and nearly destroyed Netscape. It bundled Office into enterprise agreements. Then the cloud unbundled everything — best-of-breed SaaS ate Microsoft’s lunch, one category at a time. Then Microsoft bundled Copilot into Office 365 and made the entire suite AI-native in a single pricing move. Standalone writing tools, transcription services, spreadsheet add-ons — they’re now competing against a feature inside software their customers already pay for.

Each point solution is now one much closer to becoming a feature.

AI Acceleration

The pattern accelerates when the cost of building adjacencies drops.

A CRM company that once needed a three-year engineering roadmap and $50 million to enter the HR software market can now explore that adjacency in months. A customer success platform can build product analytics features it previously had to partner for. A financial software company can add workflow automation it would have needed to acquire.

This changes who is a competitor. It changes how fast the competitive landscape shifts. It changes what “safe” means for a point solution vendor whose entire value proposition lives inside a single category.

There’s a useful analogy from military history. When a neighbor’s territory gets attacked, the pressure moves even if the attacker isn’t coming for you directly. Refugees, resource strain, alliances, and border stress. The second and third-order effects are real before the threat is direct. In software: when AI attacks the economics of one category, the players in that category move laterally. That lateral move may land in your market before you see it coming.

The Depth-vs-Horizontal Decision

Every company facing a bundling cycle has to make the same decision: go deep or go wide.

Going deep means becoming the undisputed authority in a narrower domain. The moat is expertise, data, and integration density. These things are hard to replicate even when expansion costs drop. Going horizontal means expanding into adjacencies while the cost of doing so is low, capturing territory before competitors do.

Two companies illustrate the decision differently.

GitLab sits on a genuinely defensible position: pipeline ownership, code repository history, deployment telemetry, developer trust built over years of daily use. That’s a data moat, not just a brand. The greenfield tier question — what could you attempt now that you couldn’t attempt before — opens serious expansion options: developer productivity intelligence competing with LinearB and Jellyfish, AI agent orchestration for engineering teams, continuous compliance posture management competing with Drata and Vanta from inside the development workflow.2 Every one of those expansions builds on data GitLab already owns. That’s the depth-first bundling move.

Cloudflare is the horizontal version of the same thesis. The company started as a CDN and DDoS protection point solution. Then it expanded into DNS, serverless compute (Workers), object storage (R2), databases (D1), AI inference, and Zero Trust security with each expansion built on the same global network infrastructure. Cloudflare didn’t become a different company with each move. It became a wider version of the same company. The moat is the network; every new product is just another thing the network can do.

The risk is the same risk that destroyed value in every prior bundling cycle: expansion into categories that require new buyers, new trust relationships, and new data. The railroad companies that failed weren’t the ones that went deep. They were the ones that bundled into areas where they had no natural advantage and had to build everything from scratch. The data advantage is a moat. Any expansion that builds on it is lower risk. Any expansion that abandons it is higher risk regardless of how large the adjacent market looks.

Now what?

To bundle, or to become bundled.

The great bundling isn’t something being done to you by your largest competitors. The greenfield tier runs in both directions. You can be absorbed by a platform that expands into your category. Or you can move into adjacencies where your data, your relationships, or your integration position gives you a natural advantage that a new entrant couldn’t replicate cheaply.

The companies that recognize the cycle and position intentionally will be the ones standing when the next unbundling begins. And there will be a next unbundling. But, let’s first survive the bundling phase.

You don’t have to be the one doing the bundling. But you should know which side of it you’re on.

Epilogue: This is the final post in The New Cost of Everything. If you’ve read all five, the argument in full: AI has created a new tier of value: greenfield, not just efficient or effective. That tier changes the math on shelved projects, reshapes workforce decisions, creates an absorption problem for mainstream users, and is triggering a bundling cycle that hasn’t finished running. I see many companies that are failing at one or more of these five dimensions.

The series: Post 1 · Post 2 · Post 3 · Post 4 · Post 5

Notes

- By 1890, the consolidation of shortlines into trunk lines created a hyper-dense network where rural isolation in the grain belt was effectively eliminated. Quantitative economic analyses indicate that the expansion of the rail network was the primary driver of Midwestern agricultural land improvement, bringing almost all commercial farms into direct spatial access to national markets (Atack & Margo, 2011; Donaldson & Hornbeck, 2013). ↩

- GitLab and Cloudflare expansion analysis is my own applied synthesis based on publicly available information about each company’s platform, data assets, and competitive positioning as of early 2026. It represents directional analysis, not inside knowledge of either company’s roadmap. Also, don’t use it to make investing decisions. ↩